Owners of first-party data are pioneering new and different sets of technical solutions to old advertising and marketing use cases. It is merging two markets previously separate, together as one. The results are expected to be something the industry has been waiting almost two decades for. A step-change in performance of digital marketing and advertising. And it’s all thanks to consumer data privacy legislation.

Note: This is the 3rd and final essay in a series. First was “Always On” a deep dive into real-time use cases and apps for streaming data. Then zoomed out on Marketing/Advertising GTM strategies of the Cloud Data Warehouses with “Beginning of the Endpoint.” This piece “Singularity” goes the last mile exploring the market forces around first-party customer data.

Tl;dr: Convergence of AdTech and MarTech is a data story. A first-party data story.

To explore why AdTech and MarTech are converging we need to first understand what kept them apart. It’s the same thing that’s bringing them together now, data. To date, advertising data, site behavioral data and online/offline purchase data have been collected, saved, managed and analyzed separately and differently. Siloed! And for a good reason. Data is a competitive business and product advantage.

The more brands/advertisers know the more efficient they can become with their spends. However advertising makes its margin on inefficiencies. Nothing in AdTech was more inefficient than third-party (3P) data. Efficiency is a critical point in convergence and something that differentiates AdTech from MarTech. Marketing is about efficiency and optimization e.g. finding the right balance of performance and volume. Advertising is about tonnage thus never really knowing what is working. Of course, knowing is better.

Who’s on 1st, Who’s 2nd, I Don’t Know is on 3rd Party Data

I got into AdTech from MarTech specifically because of data quality. Data quality gets too little attention but it is something I obsess over because it directly correlates with performance. 1P data is a controllable resource. You get smarter over time with it.

At Offermatica/Omniture Test&Target we OG pioneered MarTech using first-party (1P) data to optimize conversions through segmentation, testing and targeting. In 2008 after I saw aQuantive and DoubleClick get purchased for a combined $10B I left MarTech for AdTech to build an ad network using first-party data.

Ad Networks using 1P are the only thing that can really drive conversions (however you define them) in digital. It is why the platforms are the platforms. The open web AdTech market sold on an impression basis mostly against reach & frequency metrics was increasingly using third-party (3P) data. It didn’t not like performance metrics or selling cost-per-click (CPC).

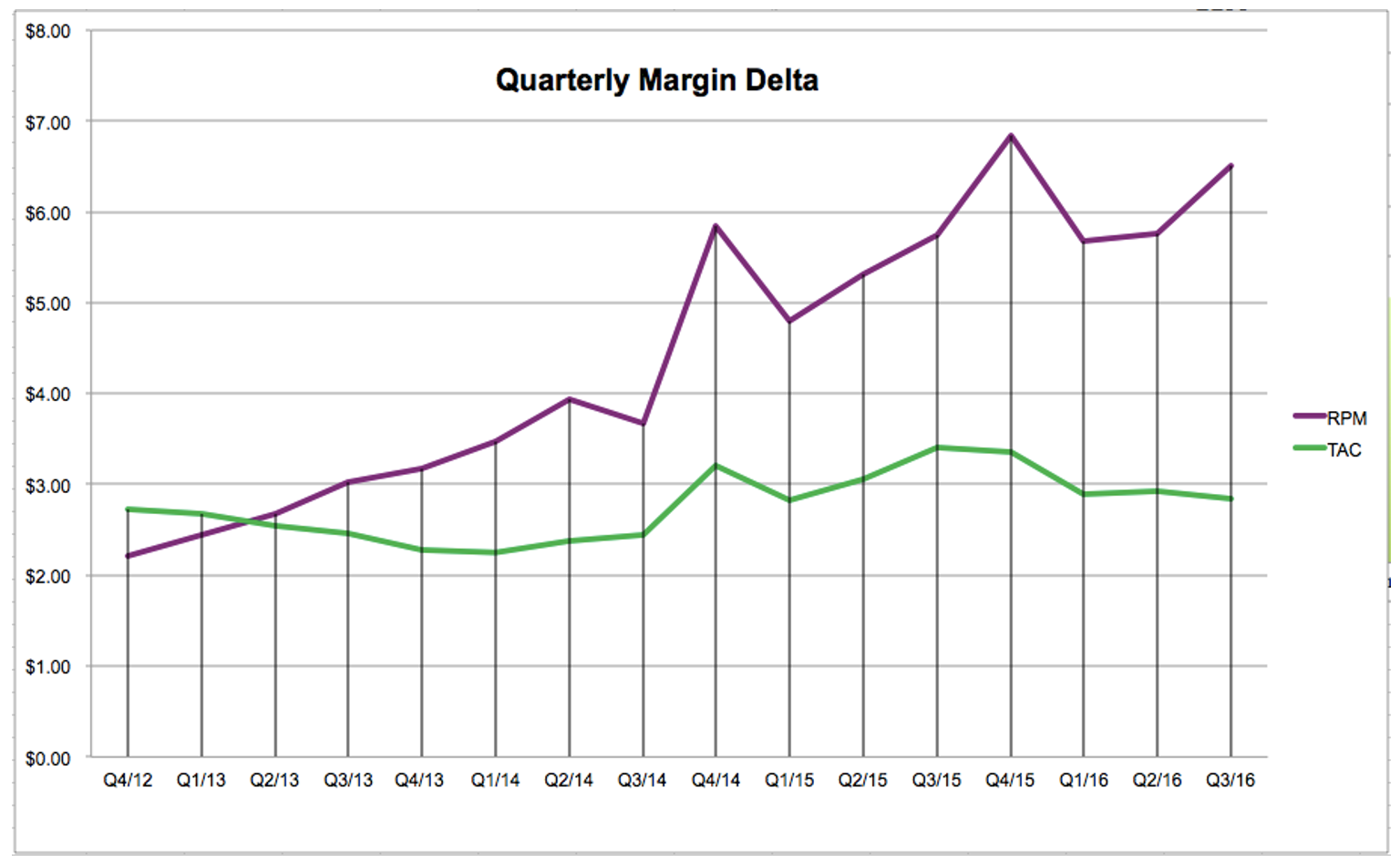

Using 1P data we outperformed every other display channel. We even outperformed syndicated search and on a few occasions even AdWords. I’ve never shared this chart until now but here is a snapshot of Yieldbot’s first 4 years of performance of Revenue (typically CPC x CTR) and TAC (what we paid publishers for impressions).

To me this chart always showed what 1P data and ML to build a performance flywheel looks like. Our performance went up as we collected more data. And not just our performance, our clients’ performance went up. As Tim Armstrong used to say “we helped our customers’ customers.” Only possible with first party data.

1P data enables direct value exchange. In addition to advertiser performance our unit pricing and volume to publishers went up too. FIrst party data is data that can be optimized to the point of diminishing returns, which there always is.

Clean Up on Aisle 3

The benefits of 1P data to AdTech are many. Data is a motor sport and 1P is streaming/real-time. 1P can be safely and securely acquired. Thanks to legislation around consumer data rights and protections the world over, a day, many years in the making has arrived. If you have been off the grid the past few years it’s important to know. This whole first-party data party is because of consumer data protection laws. Laws ironically AdTech fought every step of the way.

The digital advertising world needed to be cleaned up. Anyone deeply involved knows it is far worse than anyone has let on. Even exposed fraud did little to change things. AdTech is an industry where there are two companies worth a combined $3B whose sole use case is to prove your ads are actually being sold the way they were bought. Ad verification is just one AdTech tax. Some say it is the cost of doing business. I say server-to-server 1P data will soon eliminate these taxes. Your margin is 1P data’s opportunity.

If consumer privacy is the golden spike that connects Adtech and Martech then Clean Rooms are the first train running on the tracks. While Clean Rooms are emergent we’re already seeing pushback that their privacy related features are not all they’re cracked up to be. Legacy AdTech will not go down without a fight.

In the AdTech world huge swaths of 3P data was collected from sites by things like “Like” and “Share” buttons as well as comments systems and link shorteners. Everyone got in the consumer data game. It was a money card. If you had javascript on a website you had a data business.

This data leakage is one reason premium publishers fared so poorly with the rise of AdTech and crappy publishers fared so well. Those tags dropped cookies and pixels on consumers that collected their web behavior and sold those “audiences” to match ads against. Targeting was used to find those same people on sites with much lower price points. In ecommerce data leakage from tags created “lookalike” audiences retailers would purchase. 3P data was the wild west.

Retargeting and Attribution products had their own data issues for brands. Namely lack of data transparency. Black boxes led to cookie bombing for view-through attribution and click data injections into analytics. I recall speaking with the CPO of one of the largest attribution products after their acquisition closed. Over a few beers he mentioned to me their product never really worked but everyone wanted to believe it worked so it worked.

But Advertising does work! I am a huge fan of it. This has been studied for generations and the science can’t be questioned. The greatest artists, Warhol, Dali, Hemingway and Henson have worked in the field. Consumers see advertising, respond to advertising and purchase. Not every time but enough to fuel an $800B global market. This market now fuels a global eCommerce market. eCommerce is worth $3T today and expected to rise to $5T by 2026. Let us not forget who pays for digital ads. This is a critical point in convergence.

1P = ID

Google is probably the ultimate example of data advantage as well as what is possible with convergence. It maintains a giant data advantage because its data is not siloed. Google has first party data from it’s O&O properties (Search, YouTube, Maps) as well from your browser/client (Chrome). It also processes data from other data collectors through Google Tag Manager as well as its own data collection products Google Analytics and Firebase. You could say Google is the original Customer Data Platform (CDP) and you would not be wrong.

Google strategically and purposely built products and applications across the data spectrum that were able to join data to a single user ID. What is also interesting is that despite having the infrastructure and Google Cloud Platform (GCP) to let others build the same they did not. The first wave of CDPs were built on much more robust and analytics focused providers like AWS and Snowflake. In retrospect, that GCP could have led but stayed behind and is now playing catch up.

This leads us to the real beginning of convergence. CDPs.

CDPs changed everything by being able to stitch consumer identity together for brands from different datasets and databases. The “Customer 360” (C360) collected from first-party data (and a few strategic enrichments) was a game changer.

I’ve written a lot about the rise in CDPs going back to 2018 so I’m not going to rehash all that here. What’s important for convergence is that CDP started AdTech<>MarTech convergence by converging data about marketing and advertising, data about behavior and transactions, data about anonymous and known customers.

CDP vendors – now being called Integrated CDPs – were made possible (and built on top like every other product in MarTech) by advances in cloud computing. Advanced analytics databases like Snowflake, Databricks, Redshift and data processors like Kinesis and Apache Kafka and Spark sit at the core of CDP use cases. CDP vendors came to the fore in the years before COVID. However, until recently many kept their Customer 360 tables and SQL queries in their databases.

During COVID Composable Customer Data Platforms or cCDP emerged as a platform for owned 1P data as well as enrichment, activation and collaboration securely and with full data visibility in the cloud. I discussed composable CDP at length in a guest post on Alex Dean’s Substack here. Alex, Founder/CEO of Snowplow is another high quality data obsessive compulsive who came from the world of AdTech to MarTech.

1P + 1P = 3

CDPs and the C360 sit firmly in MarTech. However the data is influenced and enriched quite a bit by Advertising. Traffic acquisition, its cousin attribution and its father segmentation/audiences are all modeled on a C360. However since media spend is the key denominator in those formulas many CDP use cases sit firmly in AdTech. It’s no surprise to me that one of leading CDPs, mParticle, was founded by the x-AdTech data obsessive compulsive duo of Michael and Andrew Katz.

For the better part of two decades 3P data was a key value creator in AdTech for brands. But it was a dataset acquired and was controlled by middlemen. Now that it’s disappearing due to growing data privacy requirements, depreciation of 3P data and dwindling browser support for more nefarious techniques like fingerprinting.

In response to consumer data privacy protections and sensing further data advantage Google and Apple quickly started walling off data. Management of 1P became table stakes and enablement/activation/collaboration a privacy feature rather than a bug.

1P data is the new value creator in AdTech but 1P data is a MarTech thing. As these 1P C360 datasets increase in value they live in the brand cloud (increasingly Snowflake) and are owned by the brand. If convergence has a north star it is data ownership. Today I can have my golden customer record sitting in my cloud. It updates in near real-time (or once a day for most). I use this dataset to solve a myriad of use cases both internal and for my customers. And I can take this file and share it in a privacy protecting manner with partners and my partners can do the same with me.

With individual 1P datasets growing in value bringing those data sets together creates even more value. Media by its very nature has a direct relationship with audiences. Brands by its very nature have direct relationships with customers. The ability to unbundle the black boxes and collaborate via APIs and servers is changing the future of advertising and marketing. The black boxes are graying out.

Coming Clean

Sharing 1P data is made possible with Clean Rooms using privacy enhancing technologies. It is here where we really begin to see convergence playing out. Clean Rooms are a perfect tool for the Cloud businesses of GCP and AWS to collaborate with advertisers buying on two largest ad platforms in the world, Google and Amazon. In the new world everyone wants the data that is just an API call away!

Ads Data Hub is Google’s version of a Clean Room. Amazingly it was launched almost six years ago for mobile measurement of YouTube ads. Seemingly the initial use case when launched was view-through conversions from YT and GDN. Advertisers connect their transactional data in BigQuery via the Ads Data Hub API to a Google run BigQuery instance that had all the campaign data from Google. While this came to market as a “Hub” it was really just an API.

In October last year, Google decided that use cases for measurement and marketing were differentiated enough that it required creating two distinct solutions of Ads Data Hub. Ads Data Hub for Marketers and Ads Data Hub for Measurement.

We can witness MarTech and AdTech convergence accelerate in Google Ads Data Hub. The coming inflection point for first-party data is called GA4. There are 5 million companies using Google Analytics and 2 million using Google Tag Manager. With the required transition to GA4 by July 2023, in order to maximize the value of this new event-based data collection many companies will desire a BigQuery instance as an endpoint for their 1P analytics data. Once you have all that event and user data in BigQuery, Ads Data Hub Clean Room is just an API away.

Amazon, who now has the second largest advertising business in the world and the largest Cloud business does not have a site/app analytics tool to collect event data. Therefore it makes sense for them to take a top-down strategy vs GCP’s bottom up strategy to fend off GCP and grow AWS.

In early December Amazon announced a suite of AWS services collectively called Amazon Marketing Cloud for their advertisers. The suite contains 5 different solutions:

- ID Resolution

- Clean Room/Data Collab

- Measurement/Insights

- Personalization

- Ad Activation

Clean room was of course a key part of this solution and overall I have to applaud AWS strategy here and their go-to-market positioning. AWS “clean rooms in minutes” as Adam Selipsky CEO of AWS presented it is a pretty compelling go-to-market. AWS and Google know the best convergence is one you don’t even realize is happening. It’s all just data!

Use Cases Bridging AdTech & MarTech

Clean room provides a way to run matching overlays and use first party data similar to what DMPs (Data Management Platforms) were/are doing. It’s no accident the team who founded Habu came out of the market leading AdTech DMP Krux (seeing a pattern here?). Clean Rooms will say they solve for all these use cases but your mileage may vary:

Audience Matching/Overlap: This is the primary use case for media companies. Advertisers and agencies have their own datasets of audience profiles. Those get overlaid against each other and activated as segments/audiences for ad matching/delivery. This also allows for the understanding of incrementality as well as frequency management.

Lookalikes/Enrichment: These are the old 2nd and 3rd party data joins now out of the DMP and into the Clean Room. Of course now it’s all magically “first-party data.” You may get enrichments like Household income, DMAs, “in-market for X” attributes etc to help you expand your audience addressability.

Attribution: Campaigns need back-end performance data. For example a CPG advertising on a RMN (Retail Media Network) could get conversion data for their SKUs matched to impression data and click data. An Auto OEM could see how their ad campaigns drive dealer level purchases. Multi-touch attribution is coming out of the black box but incrementality testing is following close behind and might blow the top off.

Customer Journey: 1P behavioral data from a site/app combined with 1P data from channels can stitch a customer journey analysis together where slices can provide deep insights on all stages of the customer lifecycle and used to create rules based content delivery aka algorithms that optimize the right message at the right time to the right person. Worth noting Adobe/Azure is very active here.

These cover most of the major marketing/advertising use cases for data with the exception of one really large need necessitated by first-party data – identity resolution. Not to be outdone by the CDPs who came to market with Identity / C360 view of the customer as their primary use case (and rightly so!) Clean Rooms also claim to stitch identity.

The Hold Out

As Microsoft/Adobe, Amazon, Google, Snowflake, Databricks and others continue to pave the way for MarTech<> AdTech convergence there are issues that could delay the inevitable. Delay is all the defenders of the AdTech market really want at this point (and I include Google in that list).

The first issue is a technical one. Speed.

AdTech for all its data privacy squabbles is actually an incredibly performative technology. I’d argue it’s the most performative web technology ever created. In the milliseconds between your click and the page loading hundreds of parties are making multiple decisions (matching and pricing) and sending those decisions into an auction where another layer of decisioning (revenue and allocation) sits.

AdTech is a massively parallel and highly distributed computational system with numerous ML applications under the hood. Additionally, over the past few years AdTech has been leading the way in server-to-server implementations – especially compared to MarTech solutions like Tag Management or Testing & Site Targeting which I would say are uncomfortably behind in server-to-server adoption.

These near real-time advertising decisions, the streaming event data and lookup tables that drive AdTech are not perfect use-case matches with the current features of the leading MarTech cloud analytics databases like Snowflake, Redshift or GCP. The need for speed/streaming in the Cloud has been focused on data pipelines not the tables themselves. This is one reason we are seeing data applications move to the edge as well as the emergence of data lakes connected to the data warehouse.

The second issue is harder to solve. People.

Advertising, Marketing and Data Engineering are traditionally three parts of the org that don’t talk to each other. When they do speak it is typically two or three different languages. AdTech Go-To-Market positioning in the world of cloud composability has been lagging.

I’ve written about this org hold-up before related to CDP GTM. With Clouds now in direct GTM in Marketing and Advertising channels the org issue is getting more complicated. When I see things like AdTech people renaming “Clean Rooms” as “Data Collaboration Rooms” I worry. When I hear MarTech people tell me their GTM is only focused on the CTO or the CDO/CIO or CMO I worry. A common language is needed, existing stakeholders need to be brought together and additional stakeholders need to be added in order for convergence to mature.

This GTM is not easy. It’s complex and it’s butting heads against an industry built on 3 Martini lunches. CDPs can do so much and by their nature should appeal to many constituents of an org. Customer data can and should be used well beyond Advertising and Marketing use-case and inform Merchandising, Forecasting, Supply-chain and more. But how do you sell a Swiss-Army Knife to someone wearing $600 sunglasses in Cannes?

The Argument

AdTech and MarTech convergence is happening whether we want it or not. Cloud is the main growth driver of Alphabet, Amazon and Microsoft. 3 of the 5 most valuable companies in the world. A 4th, Apple is also building an Advertising business and walled off its data because of privacy. Will we one day see iCloud for Brands with all the same use cases available?

The argument that 1P data helps the platforms and walls off more gardens is true. However, each garden is only as pretty as their performance. Now more data can be shared to improve performance. Also the rise in platforms over the past decade (Shopify, TikTok, Walmart, Uber) is a positive development for marketers and advertisers. The more gardens the better.

The irony is that many felt (and fought against) privacy regulation would destroy an advertising supported web. What it has done instead is spur a wave of innovation that starts with data quality and ends with improved business performance and happier customers. This is progress.

Built for the Future

Mergers and convergence are reductive by nature. The number of companies in both spaces will shrink, that was going to happen anyway. What’s important is we are now building a future proof infrastructure. This is it. At least until everything is AI and even then it will run in the cloud.

More things will move to the edge (or even the device) but data will move at higher and higher speeds, decisions will be made more intelligently and consumers will have better, more relevant experiences using the web to meet their needs. It will be amazing to see what we can accomplish technologically over the next few years as we finally put the desires of consumers over the desires of sellers and watch as AdTech and MarTech go from being two separate markets and become one. All thanks to first-party data and consumer privacy. Hooray for people and their wallets!

Leave a comment